Life insurance is one of the most important financial tools you can have. Whether you’re protecting your family’s future, planning your estate, or building long-term financial security, choosing the right insurer matters. New York Life insurance stands out as one of the most established and respected providers in the industry.

In this comprehensive guide, we’ll explore policy types, benefits, riders, dividend potential, and how to determine if New York Life is the right fit for you.

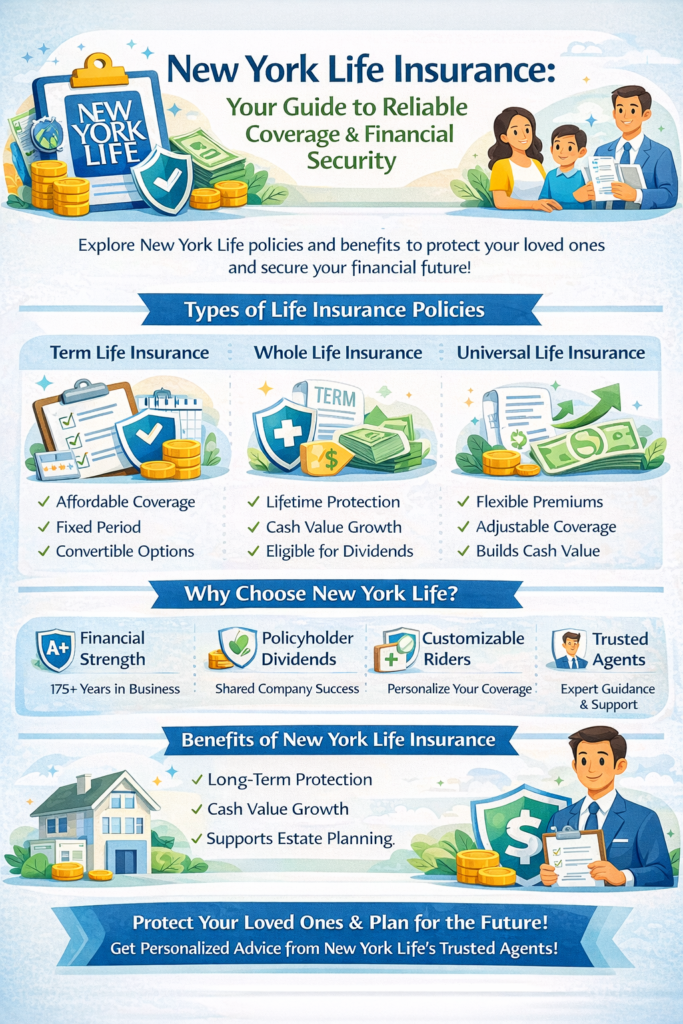

About New York Life Insurance Company

Founded in 1845, New York Life is one of the largest mutual life insurance companies in the United States. As a mutual company, it is owned by its policyholders rather than shareholders. This structure allows the company to focus on long-term financial strength and customer benefits.

Key Highlights:

- Over 175 years in business

- Consistently strong financial ratings

- Policyholder-owned structure

- Offers dividends on eligible policies

For official product details, visit the company’s website at New York Life.

Types of New York Life Insurance Policies

New York Life offers a wide range of life insurance solutions to meet different financial goals.

1. Term Life Insurance

Term life insurance provides coverage for a specific period—typically 10, 15, 20, or 30 years.

Features:

- Affordable premiums

- Fixed coverage period

- Death benefit protection

- Convertible to permanent policies (in many cases)

Best for:

Young families, mortgage protection, income replacement, or temporary financial obligations.

2. Whole Life Insurance

Whole life insurance offers lifetime coverage with a guaranteed death benefit and a savings component known as cash value.

Key Benefits:

- Guaranteed level premiums

- Tax-deferred cash value growth

- Eligible for dividends

- Lifetime protection

Because New York Life is a mutual company, eligible whole life policies may receive dividends, though dividends are not guaranteed.

3. Universal Life Insurance

Universal life insurance provides flexible premiums and adjustable death benefits.

Types May Include:

- Standard Universal Life

- Guaranteed Universal Life

- Variable Universal Life

Best for:

Individuals seeking flexibility and potential cash value growth tied to market performance (for variable policies).

Why Choose New York Life Insurance?

Choosing the right life insurance provider involves more than comparing premiums. Here’s what makes New York Life stand out.

1. Financial Strength and Stability

New York Life consistently earns high financial strength ratings from independent agencies such as:

- A.M. Best

- Moody’s

- Standard & Poor’s

Strong ratings indicate the company’s ability to meet long-term policyholder obligations.

2. Policyholder Dividends

As a mutual company, New York Life pays dividends to eligible policyholders when financial performance allows.

Dividends can be used to:

- Reduce premiums

- Increase coverage

- Accumulate interest

- Receive cash payouts

3. Customizable Riders

You can enhance your policy with optional riders, including:

- Accidental death benefit rider

- Waiver of premium rider

- Long-term care rider

- Disability income rider

- Children’s term rider

Riders allow you to tailor coverage to your unique needs.

How Much Does New York Life Insurance Cost?

Life insurance premiums depend on several factors:

- Age

- Health status

- Smoking history

- Coverage amount

- Policy type

- Gender (in some states)

Term life insurance typically offers the lowest initial cost. Whole life and universal life policies are more expensive but include lifelong protection and cash value accumulation.

Term vs. Whole Life: Which Is Right for You?

Choosing between term and permanent life insurance depends on your goals.

Term Life May Be Better If:

- You need affordable coverage

- You have temporary financial responsibilities

- You want income replacement during working years

Whole Life May Be Better If:

- You want lifelong protection

- You’re interested in building cash value

- You want potential dividend participation

- Estate planning is a priority

Benefits of New York Life Insurance

Here are some major advantages of choosing New York Life:

Long-Term Financial Protection

Provides security for:

- Mortgage payments

- Children’s education

- Outstanding debts

- Final expenses

Cash Value Growth (Permanent Policies)

Whole and universal life policies accumulate tax-deferred cash value that can be accessed through:

- Loans

- Withdrawals

- Policy surrender

Estate Planning Support

Life insurance can:

- Cover estate taxes

- Provide liquidity for heirs

- Equalize inheritance distributions

How to Apply for New York Life Insurance

Applying typically involves:

- Choosing the policy type

- Determining coverage amount

- Completing an application

- Undergoing medical underwriting (if required)

- Receiving approval and policy issuance

Some policies may offer simplified underwriting options depending on eligibility.

Is New York Life Insurance Worth It?

New York Life may be ideal if you value:

- Financial stability

- Long-term guarantees

- Dividend potential

- Personalized service through agents

However, it’s always wise to compare multiple insurers before making a decision.

Comparing New York Life With Other Insurers

When evaluating life insurance providers, consider:

- Financial strength ratings

- Customer satisfaction

- Policy flexibility

- Dividend history

- Premium affordability

Shopping around ensures you find the best coverage for your needs and budget.

Common Mistakes to Avoid

When buying life insurance, avoid these pitfalls:

- Buying too little coverage

- Waiting too long to apply

- Focusing only on price

- Ignoring riders

- Not reviewing your policy regularly

Life insurance needs change over time—review your coverage periodically.

Internal & External Resources

For further reading:

- Check our guide on Term vs Whole Life Insurance Explained (internal link)

- Explore our article on How Much Life Insurance Do You Need? (internal link)

- Visit New York Life for official policy details (external link)

Final Thoughts: Securing Your Family’s Future

New York Life insurance offers a wide range of coverage options backed by over a century of financial strength and policyholder-focused service. Whether you need affordable term life insurance or permanent coverage with cash value benefits, New York Life provides solutions designed for long-term security.

Before purchasing any life insurance policy, evaluate your financial goals, budget, and family needs. Compare quotes, understand policy features, and consult a licensed agent if needed.